Subscribe to Our Newsletter

Hear more from Equity Methods: Your trusted partner in equity compensation excellence.

This is an expanded version of an article originally published on October 16, 2024 on the NASPP Blog.

In the world of equity compensation, different companies have different structures. A corporation typically issues options or shares. A partnership or LLC, on the other hand, might issue profits interest units (PIUs).

Like other forms of equity compensation, PIUs allow the holders to participate in the company’s future growth, typically in exchange for services to the company as employees. That participation includes profits from operations as well as distributions and future appreciation in the asset values.[1] Another similarity is that PIUs are intended to align employee interests with building value for the company and achieving its business goals.

Unlike other partnership units, PIUs don’t require an upfront capital contribution from the recipients. Payment to all units in the partnership follows a tiered waterfall, and these units fall junior to any other capital units that have an associated capital contribution.

Profits interests fall into two general categories, as discussed in our recent coverage of ASU 2024-01:

Some units may have both features, but in this discussion, we’ll consider them separately.

In all cases, profits interests are issued, rather than sold, to holders, with a $0 liquidation value on the date of issuance. In other words, if the company is sold on the date the units are granted, the interests would receive no value, akin to an option granted at-the-money. This is different from a capital interest, where a recipient pays into the partnership to receive a unit and may obtain a return of value, even upon an immediate liquidation.

As we mentioned, there are two ways holders receive value—based on a company’s earnings or based on an increase in equity value. The first is like a bonus plan, whereas the second is classified as equity compensation.

Distributions to PIUs based on investor proceeds upon a future liquidity event resemble a call option on the company value. That’s because they receive no distributions until the required capital distributions are made to all other capital units (typically a reimbursement of contributed capital with a level of profit). Often, PIUs are subject to an additional, higher threshold before they receive value, similar to performance shares and options. For example, they might be eligible to receive value only if the capital units receive double their initial investment. These hurdles result in a lower value to the holders.

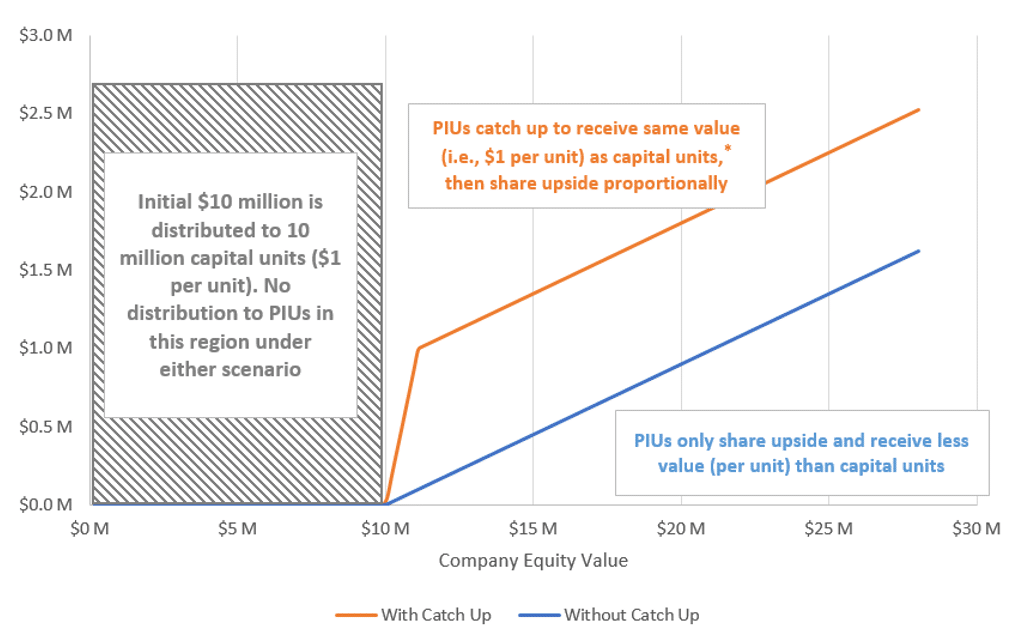

There are two payout profiles, both resembling other forms of equity compensation. To see how they pay out, suppose there’s a transaction above a threshold value of $10 million for the company. The PIU shown by the chart’s blue line is option-like, meaning it shares in value dollar for dollar with the capital interests. On the other hand, the PIU reflected in the orange line vests based on the threshold but results in a higher value unit when vested. These are similar to full-value shares and are incorporated by “catching up” the share value on vesting.

Payout Comparison for Profits Interest Units

*The distribution threshold here is assumed to be $1 per unit. This may also be different than the per-unit capital contribution. For example, if a 2x return to the capital units is required for payout, then the distribution threshold would be $2 per unit. Similarly, the distribution threshold may also be lower than the per-unit capital contribution.

The valuation of PIUs takes these hurdles into account, typically by looking at the PIUs as a combination of call options on the full equity value of the company. The Option Pricing Method (OPM) is often used to calculate the fair value of these units. The OPM uses the same assumptions[2] about the distribution of equity value of the company at a future liquidation event as the infamous Black-Scholes model and applies them to value each share class. In other words, the OPM treats each class of shares as call options on the equity value, with the relevant liquidation preferences, or hurdle amounts, as the strike prices.

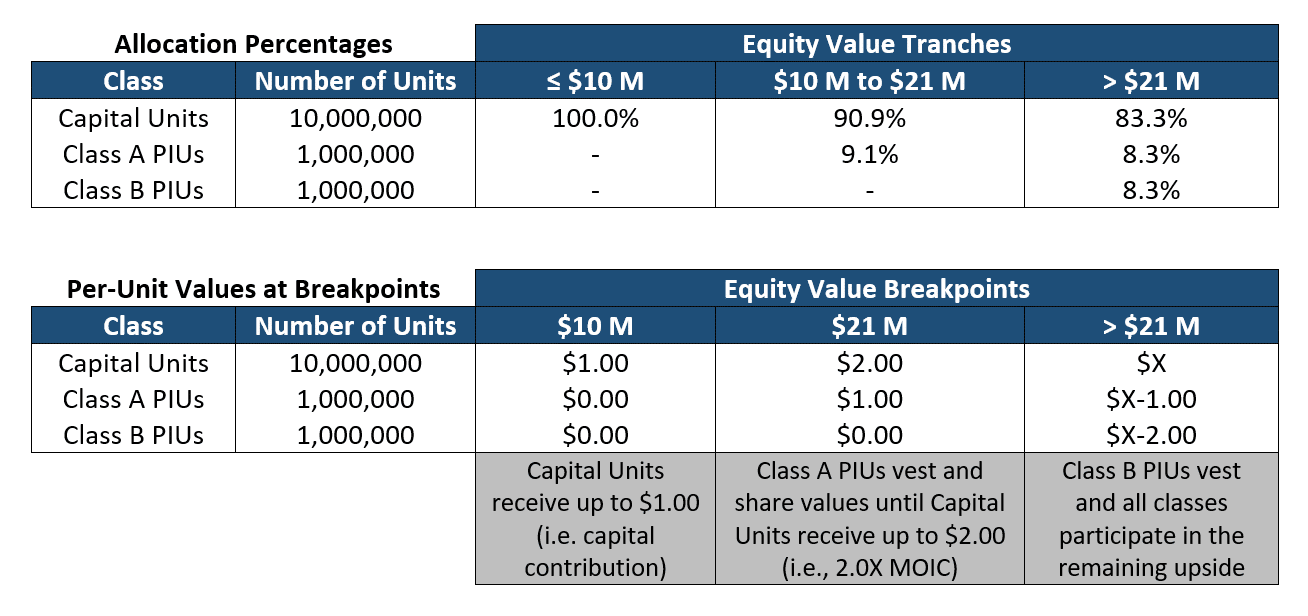

For example, let’s say we have a company that received a $10 million capital contribution from investors in exchange for 10 million Capital Units. Subsequently, the company issued 1 million Class A PIUs that vest at liquidation if the Capital Units receive their contributed capital and 1 million Class B PIUs that vest at liquidation upon a 2.0x return to the Capital Units. The OPM creates three buckets of future equity values and distributes them as follows:

Based on the above distribution percentages and equity value breakpoints, the OPM can be used to calculate the fair value at each breakpoint with the Black-Scholes model and strike price as the equity value breakpoints, asset price as the equity value at the valuation date, term as the time to liquidation, volatility as the expected equity volatility of the company, and the risk-free rate as the growth rate for the equity value.

The value for each tranche is calculated as a piece of the overall equity value, with all such pieces adding up to the total equity value. The value of each tranche is then equal to the difference between the fair value at the lower breakpoint (for the first breakpoint, we use the total equity value) and the upper. Those with option experience may have seen this referred to as a “bull call spread,” where the payoff is stable at zero below the lower breakpoint, the maximum at the upper breakpoint, and moves one-to-one with the stock in between. To value an individual class, we multiply the class’s allocation percentage for each tranche by the value of the respective tranche and sum up all such values.

The relevant accounting standards and expense can differ substantially depending on the type of PIU. ASC 718 is applicable to the ones where profits are based on either the growth of the entity’s overall market value or the return of capital to the investors. Even if the vesting itself isn’t based on market value, but the distribution of proceeds is, the units would still be accounted for under ASC 718.

In this case, there are three primary accounting treatments.

In other cases, the company’s equity value doesn’t determine remuneration for the PIUs, as when payout is based on the company’s accounting measures (such as operating profits or earnings). For example, the pool of profits interest may receive 10% of the company’s net operating profits, after tax, after the first $10 million. This is like an earnings-based compensation plan. The guidance from Accounting Standards Update (ASU) 2024-01 indicates the use of ASC 710 (Compensation – General).

To gain favorable tax treatment, PIUs are issued such that they have a $0 liquidation value as of the issuance date. This means that, analogous to an at-the-money option, the value received by the PIU holder is zero if the company was immediately sold as of the grant date. All value is based on future profit or upside value.

This allows for the use of a safe harbor under tax law. Under typical conditions, a PIU recipient can make an 83(b) election. An 83(b) election allows recipients to pay tax on a grant at the time of issuance, rather than at vesting, and set a cost basis accordingly. For PIUs, due to the lack of a liquidation value, the value at the time of issuance for taxes is considered to be $0. Thus, no tax is due at grant, assuming the following conditions are met.

Further, assuming the holding period is longer than two years, the holder will typically be taxed on all proceeds at the lower capital gains rate.

It’s worth noting that if a PIU is held for more than two years, the IRS guidance assumes that a deemed 83(b) election has been made, although most recipients still explicitly make these elections.

For public companies, accounting for and administering an equity plan can be significantly aided by software systems geared toward their needs. However, at a private company, data may be very closely held. That raises the risk of asymmetries. To avoid information gaps that result in financial reporting deficiencies, we help clients establish the necessary data templates and lines of communication for PIUs. Given the diversity of stakeholders involved, proper access controls are critical to program confidentiality.

For more information, please reach out to the authors.

[1] To learn more, see IRS Revenue Procedure 93-27, 1993-2 C.B. 343 and Revenue Procedure 2001-43.2001-2 C.B. 191.

[2] This is discussed in further detail in our Issue Brief “Your Piece of the Pie: Understanding the Valuation Impact of Multiple Share Classes”